How's Business? Survey July 2022

- Home

- Media Centre

- Spotlight Features

- How’s Business? Survey July 2022

Introduction

“As we did throughout the pandemic, Marketing Lancashire continues to work closely with colleagues at Visit England and DCMS, sharing business intelligence and highlighting the challenges that the sector faces here in Lancashire. Despite the resilience and determination shown by Lancashire’s tourism and hospitality businesses, it is clear that yet more difficult times lie ahead as the cost of living crisis impacts both businesses and consumers, restricting any hoped for return to growth. It is vital that we track impacts and share that data with Government, and we thank all the businesses who took the time to respond to this survey.” Rachel McQueen, Chief Executive of Marketing Lancashire

An online survey was conducted between 27th July and 3rd August 2022 to collect insights into tourism and hospitality sector performance across the 2022 year to date. Headline findings are outlined below.

Overview and Headline Results

- Looking at the year to date (January – July 2022), the sector has still seen levels of both visitor numbers and business turnover suppressed with over half of respondents reporting visitor numbers / footfall down compared to usual (pre-Covid levels), accompanied by a drop in business turnover.

Those reporting a rise in numbers accounted for approximately one third of respondents whilst just under a quarter of respondents stated that business turnover was up.

- The potential boost over the Jubilee Weekend and Spring Half Term period did not appear to have materialised as hoped – although around one quarter of businesses saw some increase in visitors and turnover, a greater majority (63%) saw some drop in footfall and visitors and a lower turnover (47%).

- Resulting business confidence is mixed going forward; just 12% of respondents stated they felt very confident about this summer, with 35% somewhat confident and a further 35% feeling unsure. 18% stated either they did not feel so confident or not at all confident about summer trading.

In general, when asked about their ability and confidence to trade going forward, there was greater confidence looking over the short term this year with less certainty looking further ahead over the next 2-3 years.

- The main factors affecting business were clearly reported as economic ones with 91% stating high energy / fuel costs were affecting business most, followed by 82% quoting the challenging economic climate and less disposable income / money in consumer pockets. 82% also stated rising supplier costs were a major factor affecting business.

- Businesses reported the current economic climate and lower levels of consumer spending (54%) as their main concern. In response to rising business costs, a range of business responses had been implemented; most commonly, over half (57%) of business had increased prices by up to 10% and a further 14% had increased prices by over 10%. A significant level of businesses (34%) also reported that they had responded through cutting other costs by delaying investment, building or maintenance works.

- In terms of staffing and recruitment, when asked what percentage of staff vacancies the business currently had, a high proportion stated 0% with just a couple of respondents stating that 5% of positions were vacant and a couple more reporting 10% of positions being vacant. The leading areas of business operation reported to have vacancies were front of house / reception, housekeeping, chefs (all 15% each), followed by bar and waiting on staff (12% each). In terms of recruitment, 44% said that they found recruitment challenging for some types of roles (although these were not specified) with a further 16% reporting challenges in recruiting seasonal roles. The most significant factors affecting recruitment were a lack of applicants and skills shortages – lack of suitably qualified / experienced applicants. In response to these challenges, over half of business respondents had increased salaries (54%), followed by training incentives (33%), improved hours / shift patterns (21%) and improved benefits (17%). 12% had also offered accommodation for staff.

Visitor Numbers and Business Turnover – Year to Date

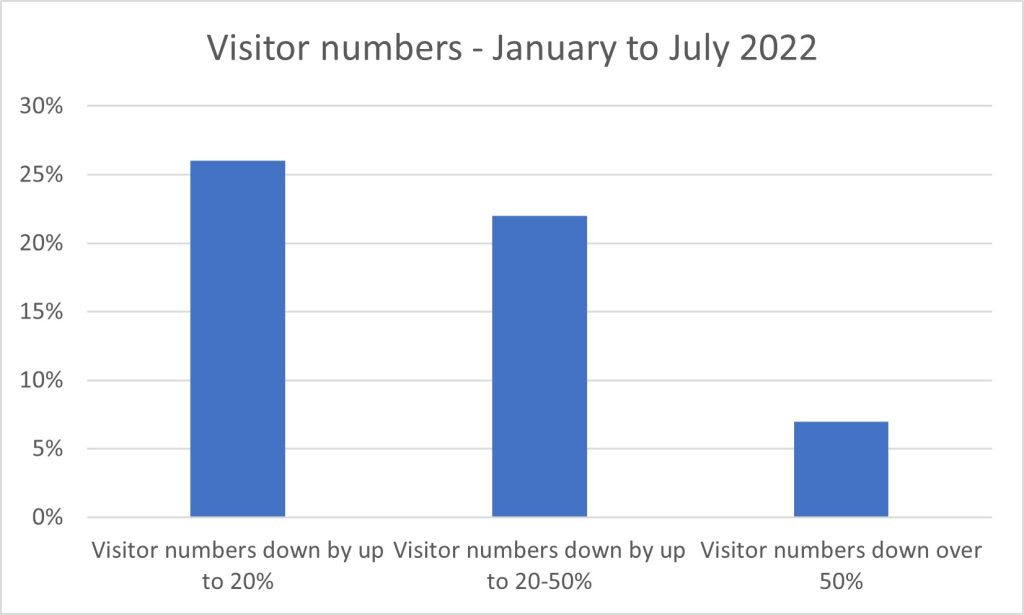

- Between January – July 2022, over half of respondents reported that visitor number / footfall was down compared to usual (pre-Covid levels). Approximately one quarter (26%) of all survey respondents stated that visitor numbers were down by up to 20% followed by a further 22% who stated visitor numbers were down between 20-50% and 7% who reported numbers to be down over 50% compared to usual.

- 15% stated that visitor numbers were on a par with usual levels and just under one third showed an increase in visitor numbers comprising 19% who saw an increase up to 20% more; 7% respondents who saw an increase between 20-50% and 4% who reported an increase over 50% on usual levels experienced pre-Covid.

- With regards to business turnover across the same period, a similar pattern was observed with the majority (63% of total respondents) reporting a fall in turnover. One third (33%) stated turnover was down by up to 20% with a further 20% of respondents reporting business turnover to have fallen between 20-50% and 10% stating a drop of over 50%.

In contrast, just under one quarter (23%) reported an upturn with 10% stating turnover had increased by up to 20%, a further 10% between 20-50% and 3% stating turnover was up by over 50%.